{kind=link}

Subprime auto loan asset-backed securities investors should bow their knees in front of US taxpayers to thank them for the backdoor bailouts.

By Wolf Richter for WOLF STREET.

Subprime auto loans are risky but very profitable as they carry high rates even during times of insanely low interest rates. Much of the risk is shifted onto investors by securitizing those loans in sub-prime auto-loan-asset-backed securities (ABS) that are cut into tranches of the highest creditworthiness that take the most recent loss but the the lowest-rated tranches that take the first losses but generate the highest returns. There is something for everyone.

Collecting vehicles is generally quick and easy, with few hurdles and a very liquid auction market to dispose of the vehicles efficiently. Professional repo companies get the vehicle, clean it and bring it to auction. For subprime lenders, it’s all pretty smooth.

For example, subprime auto loan defaults of 60 days and more, securitized in ABS and rated by Fitch, have been rising for years as lenders took more risk amid institutional investors’ voracious appetite for subprime auto loan ABS. In 2016, the over 60-day default rate exceeded the highs during the financial crisis. In August 2019, it matched the October 1996 peak, the worst in the data. And in January and February 2020, the failure rate rose through the worst January and February ever. So it was going in the wrong direction. And then came the Voices.

In May 2021, the default rate of over 60 days for subprime auto loan ABS fell to 2.58% of total auto loans (“prime” and “subprime” combined) according to Fitch Ratings. This was the lowest rate since 2012, when defaults decreased because by then the overdue loans had been written off and cleared from the system from 2009-2011 and lenders had become cautious with new loans.

Fitch’s ABS default index for prime auto loans, which remained below 1% even during the financial crisis, fell to an all-time low of 0.14% in May.

Apparently some of the voting was used to catch up on overdue car loans. And that didn’t help the economy or jobs or whatever, but it did help lenders and investors who otherwise might have suffered huge losses on their subprime loans and ABS.

So those Texas, California, or Norway pension funds and their beneficiaries should bow their knees to the voters and the U.S. taxpayers who paid for those backdoor bailouts.

But at the same time, car buyers with subprime credit scores – below 620 – have stayed away from buying a vehicle, maybe put off by the insane new and used car price increases or maybe because they still haven’t got a job.

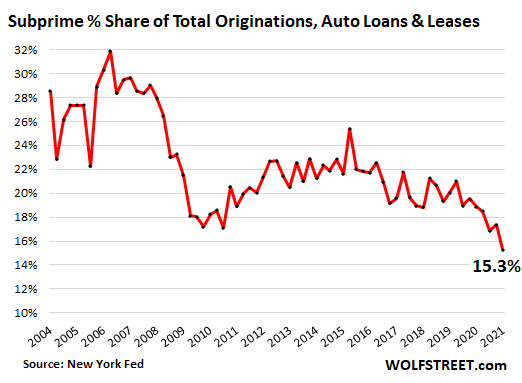

According to the New York Fed’s Household Debt and Credit Report, the percentage of subprime-rated loans and leases issued fell to 15.3% by loan amount in the first quarter of 2020, the lowest in 2004 data, a further confirmation of the -formed recovery:

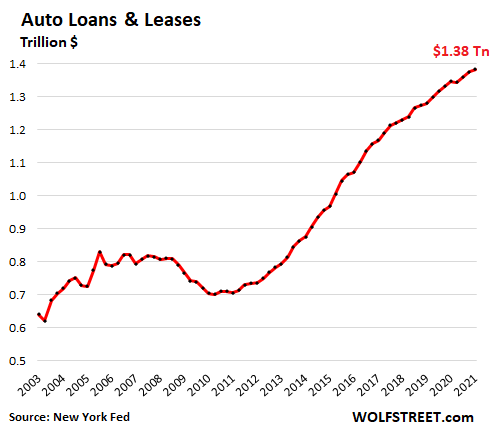

At the end of the first quarter there were $ 1.38 trillion in auto loans and leases outstanding, 2.7% more than a year earlier, the lowest year-on-year growth since 2011, despite massive increases in the price of new and used vehicles that would have borrowed amounts lifted up. This could be further confirmation that more people have paid cash and perhaps have poured their stock market profits into the economy; and that more potential customers with below-average ratings are on buyers’ strike because they either do not want to or cannot buy at these prices.

Have fun reading WOLF STREET and would you like to support it? Using ad blockers – I totally understand why – but want to support the site? You can donate. I appreciate it very much. Click on the beer and iced tea mug to learn how:

Would you like to be notified by email when WOLF STREET publishes a new article? Login here.

![]()